Tuesday, May 31, 2011

Part Three - Other Endorsements & Umbrella Policies

In part three, the final section of our video on homeowners insurance, we discuss other important homeowners endorsements, liability coverage, and umbrella policies. Special guest appearance by Jackson Allen Bagley, creator of JAB Productions. Onward and upward!

Saturday, May 28, 2011

Desires and satiety

While the content here is somewhat focused on personal finance, I think it's beneficial to step back and examine the various things that impact our happiness the most. People often seem to be just as ill-advised about what really makes them happy as they are about how to handle their finances. It's a platitude to say that money doesn't buy happiness, but some work in behavioral finance has shown how true this statement is. Jason Zweig explains:

In 1957, the average American earned about $10,000 (adjusted for inflation) and lived without a dishwasher, clothes dryer, television, or air conditioner. But 35% of people surveyed then said they were "very happy" with their lives. By 2004, personal income had nearly tripled after inflation, and the typical house was bursting with consumer goods. Yet just 34% of people now said they were "very happy." Somehow, almost tripling our wealth has made Americans a little less happy--and still we want more.

And we still want more. That's the key right there. Above a certain level it's quite obvious that increases in wealth don't bring much more happiness. See here for where that threshold roughly is. While I'm not big on self-help books, occasionally here we'll explore what can increase happiness, as I find that kind of research fascinating. First up: schooling our desires.

H.L. Mencken once defined a wealthy man as one who earns $100 a year more than his wife's sister's husband. A paper by Neumark and Postlewaite (1998) demonstrates just how accurate Mencken's remark really was. Investigating the effect of relative income by looking at the employment decisions of women and their sisters-in-law, they find that there's a positive effect of sister-in-laws' employment on women's own employment after taking into account common explanatory variables. They explain: "women with non-working sisters are more likely to be employed if their husbands earn less than their sisters' husbands; this result is consistent with women's employment decisions being partly driven by relative income concerns, because women with relatively low-earning husbands and non-working sisters may be able to attain higher relative family income if they work." It appears that our decisions are often largely driven by our wealth as it compares to that of our family, friends, and co-workers. These comparisons are often a large source of unhappiness.

The negative effect of relative-wealth desire on our happiness is pervasive even in relatively austere China. A 2009 paper by Knight and Gunatilaka performed a survey of roughly 9,500 households in rural China to determine the effects of income aspirations on subjective well-being. They found that "aspiration income is a positive function of actual income... and that subjective well-being is raised by actual income but lowered by aspirational income. These findings suggest the existence of a partial hedonic treadmill, and can help explain why subjective well-being in China appears not to have risen despite rapid economic growth."

Essentially, wanting makes us less happy. This has a real eastern religion feel to it, but it is also one of the key tenets of the man who was called, in effect, the quintessential American, i.e., Henry David Thoreau. In Walden he remarks that "a man is rich in proportion to the number of things he can afford to let alone." Elsewhere has says that his "greatest skill in life has been to want but little." Things often have a way of encumbering us.

Accordingly, much of my time would be better spent curbing my desires rather than trying to satisfy each of them. Raise a glass to austerity.

Monday, May 23, 2011

Wednesday, May 18, 2011

Maybe she's born with it

Outliers, Malcom Gladwell's book from a couple years back, made me start seriously thinking of how much one can accomplish in life, genes, predispositions, and innate talent be damned. A recent conversation with a professor rekindled my interest. In his book, Gladwell discusses the characteristics of those who have achieved uncommon success in life and tries to tease out what these people have in common. The gist? They've worked hard and we're born into the right situation (see Warren Buffett and Bill Gates). Buffett, for example, has cited his winning of the 'Ovarian Lottery' as playing a big part in his development as a child. This, indeed, is indisputable and we're lucky to be born into society rich enough to enable blogging and other leisures. His and Gates' skill set has been cited by some to be (serendipitously!) relevant to this era (i.e., Gates wouldn't have done as well not growing up at the beginning of the computing age), but I think one learns what's available. I don't think he wouldn't have wanted to start Microsoft having been born in the dark ages and perhaps would have advanced in some other endeavor by dint of his hard work.

But, this gives even more hope to those who might not have won the shadowy skill-set-era lottery. Generally Gladwell finds that the top performers in various fields (physics, music, baseball) haven't been born with a natural ability to perform at a high level, but rather have practiced an inordinate amount at their respective interest. He cites various studies and talks of a 10000 hour rule, which is roughly the practice threshold above which someone truly becomes a master. But, what about all those gifted students in middle and elementary school? What appears to happen is that at a very young age certain kids are seen to have a (very slight, and probably from parental influence of some sort) proclivity for a certain subject, instrument or sport. These kids are then enrolled in special classes, receive better training, and invest more practice time cause of the related encouragement. By the time most kids have taken a casual interest in such things, these "prodigies" are already years ahead of the normal kids. It's a feedback loop, of course; the normal kids are never gonna catch those with access to the special classes and heightened encouragement and the gap tends to widen over time.

While there are some barriers that preclude some from the elite, the positions of influence are more accessible than they seem (provided you've a work ethic provided you put in the hours). Gladwell cites a book which show that there are only about three IQ levels that have a big influence on one's life*. The basic point is that if you're above ~115 IQ, fortunately, hard work can get you into grad school, and from there you have a shot at the elite.

Some thoughts from one of my favorite posts on the implications of all this:

But, this gives even more hope to those who might not have won the shadowy skill-set-era lottery. Generally Gladwell finds that the top performers in various fields (physics, music, baseball) haven't been born with a natural ability to perform at a high level, but rather have practiced an inordinate amount at their respective interest. He cites various studies and talks of a 10000 hour rule, which is roughly the practice threshold above which someone truly becomes a master. But, what about all those gifted students in middle and elementary school? What appears to happen is that at a very young age certain kids are seen to have a (very slight, and probably from parental influence of some sort) proclivity for a certain subject, instrument or sport. These kids are then enrolled in special classes, receive better training, and invest more practice time cause of the related encouragement. By the time most kids have taken a casual interest in such things, these "prodigies" are already years ahead of the normal kids. It's a feedback loop, of course; the normal kids are never gonna catch those with access to the special classes and heightened encouragement and the gap tends to widen over time.

While there are some barriers that preclude some from the elite, the positions of influence are more accessible than they seem (

Some thoughts from one of my favorite posts on the implications of all this:

Today's my birthday. It got me thinking.

Do you understand the power of compound interest? And I'm not talking about finance, actually.

I started this blog about 9 months ago as a little social media experiment. 6 months ago it started taking the shape of what it is today. Now all the sudden there are over 1100 posts, thousands of people paying attention every day, a store, comments, links...

Compound interest.

You know what happens when you do something every day for two hours? In 13 years you're a Malcolm Gladwell "Outliers" genius at it. 13 years might seem like a long time looking forward, but try looking back. 13 years ago? Maybe not as long. Feels like I started this blog yesterday.

Let me get to the big point here: You are what you do all day.

That probably scares the shit out of a lot of people. And it should.

The same blog references a classic 1993 paper, wherein researchers looked at the role of deliberate practice in the acquisition of expert performance and found "essentially no support for fixed innate characteristics that would correspond to general or specific natural ability." After acknowledging the degree of expert performance some people attain as compared to normal people, they "deny that these differences are... due to innate talent." They go on to argue "that the differences between expert performers and normal adults reflects a life-long period of deliberate effort to improve performance in a specific domain." Do read the conclusion, at least.

Perfect from now on...

** Gladwell, on page 102, says the heritability of IQ is around 50%.

* Gladwell on page 79: "The "IQ fundamentalist" Arthur Jensen put it thusly in his 1980 book Bias in Mental Testing (p. 113): "The four socially and personally most important thresholds regions on the IQ scale are those that differentiate with high probability between persons who, because of their level of general mental ability, can or cannot attend a regular school (about IQ 50), can or cannot master the traditional subject matter of elementary school (about IQ 75), can or cannot succeed in the academic of college preparatory curriculum through high school (about IQ 105), can or cannot graduate from an accredited four-year college with grades that would qualify for admission to a professional or graduate school (about IQ 115). Beyond this, the IQ level becomes relatively unimportant in terms of ordinary occupational aspirations and criteria of success... IQ differences in this upper part of the scale have far less personal implications than the thresholds just describes and are generally of leser importance for success in the popular sense than are certain traits of personality and character.""

** Gladwell, on page 102, says the heritability of IQ is around 50%.

Saturday, May 14, 2011

We're floating in space

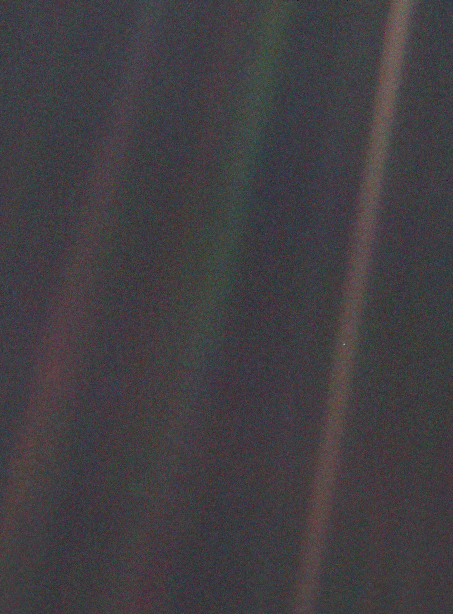

When dealing with vexing problems (whether personal, interpersonal or work related) it has lately helped me to step back and have a more complete perspective (both of space and time) in terms of my current life trajectory. This thinking has especially come to the fore in recent months (and shook me up a bit) since I found a unique photo on the web, called the pale blue dot.

In the late 1970s NASA sent a spacecraft called Voyager 1 out to take photographs of the solar system. In 1990, as Voyager was leaving the solar system (its mission having been completed) a scientist named Carl Sagan requested that the camera be turned around so it could take a picture of earth, across the deep expanse of space. The result is this image here, taken from 3.8 billion miles from earth. Stare at it for a moment.

{kind=link}

Sagan ended up titling a book after this image, and wrote the following when considering its deeper meaning:

From this distant vantage point, the Earth might not seem of particular interest. But for us, it's different. Look again at that dot. That's here, that's home, that's us. On it everyone you love, everyone you know, everyone you ever heard of, every human being who ever was, lived out their lives. The aggregate of our joy and suffering, thousands of confident religions, ideologies, and economic doctrines, every hunter and forager, every hero and coward, every creator and destroyer of civilization, every king and peasant, every young couple in love, every mother and father, hopeful child, inventor and explorer, every teacher of morals, every corrupt politician, every "superstar," every "supreme leader," every saint and sinner in the history of our species lived there – on a mote of dust suspended in a sunbeam.The Earth is a very small stage in a vast cosmic arena. Think of the rivers of blood spilled by all those generals and emperors so that, in glory and triumph, they could become the momentary masters of a fraction of a dot. Think of the endless cruelties visited by the inhabitants of one corner of this pixel on the scarcely distinguishable inhabitants of some other corner, how frequent their misunderstandings, how eager they are to kill one another, how fervent their hatreds.

Do read the whole thing. After reading Sagan's words about our lonely position in space, I was curious and found that Proxima Centauri, the closest star to the sun, is about 25 trillion miles from earth. In other words, when looking the photograph above, realize that it's more than 6000 times that vast distance (across soundless, -455°F space) before one reaches the nearest star (or alternate heat source). This gives us an idea of how precious and precarious our situation really is. The birds outside are now starting to chirp; I think they're aware of all this. Next time I'm interacting with someone, and, self-importantly, feel myself above the situation and the person with whom I'm dealing, I'll try and think of these facts.

Wednesday, May 11, 2011

Forecasting the shakes

First off, thanks for reading and thanks to those who've commented. To better quantify some of the earthquake hazards alluded to in the last post, I've been wading into the relevant literature for those who live near SLC. While there are a few papers relevant to the topic at hand (and apparently the Wasatch Fault is one of the most studied faults in the world), I'll briefly mention the predictions from a 1996 paper by McCalpin and Nishenko. The numbers here will still be centered around 1996.

Using a chronology of magnitude 7 or greater earthquakes along the 5 segments of the Wasatch Fault, they calculate (using some methods beyond the scope of this blog) the likelihood of similar magnitude quakes occurring over the next 50 and 100 years. First, over the last 5600 years there have been 16 earthquakes greater than a 7 magnitude; the average repeat time for these was 350 years. Of the 5 segments of the Wasatch Fault, they find that 4 of them ruptured between 620 to 1230 years ago. The Brigham City segment, however, has not ruptured for ~2120 years. This is somewhat disconcerting as they say it has an average repeat time (how often it ruptures) of 1275 to 2346 years (depending on the method used). The SLC segment is also suspect in that it hasn't ruptured for 1230 years and it has a repeat time of ~1350 years (see Table 6).

While that may seem abstract, the paper's abstract (oops) bluntly states that over the next 50 and 100 years, there is a 16 and 30% chance, respectively, of a magnitude 7+ earthquake occurring somewhere along the Wasatch Front. While these things cannot be predicted with anything close to pinpoint accuracy, these statistics come from the Journal of Geophysical Research (i.e., peer-reviewed science). Perhaps instead of springing for that extra-large-capacity ipad, one would be better served buying bags of wheat, rice, beans, and oats. For more perspective on these risks across the US, the USGS has some attractive figures showing the likelihood of similar events around the country.

{kind=link}

Monday, May 9, 2011

Insurance, Part One: Earthquake Coverage

The first video in a series of videos in which we will discuss topics such as finance, insurance, pop culture, and more. Enjoy!

Wednesday, May 4, 2011

Buffetting the buffeting

As per the name of this blog, it seems appropriate to address the steps from deferring consumption to investing for the long haul. The first of these posts will talk about one of the most important steps to becoming financially stable, which is establishing a sufficient cushion against a rainy day. As most have noticed, life has a way of derailing your smoothly laid plans in a hurry. But, barring those sad life events that cannot be fixed so easily, a good many of life's troubles can be dealt with by having a sizable pile of easily accessible cash. As with so many of these issues, Warren Buffett has given invaluable insight in his letters to the shareholders of Berkshire Hathaway*. This year's letter contains this valuable contribution from Warren's grandpa, here writing to his son:

Over a period of a good many years I have known a great many people who at some time or another have suffered in various ways simply because they did not have ready cash. I have known people who have had to sacrifice some of their holdings in order to have money that was necessary at that time. For a number of years I have made it a point to keep a reserve, should some occasion come up where I need money quickly, without disturbing the money that I have in my business. I hope it never happens to you, but the chances are that some day you will need money, and need it badly...So far, so reasonable. Things arise and people need cash. BUT, lately all and sundry have noticed the extremely low rate of interest paid on deposits. This largely encourages people to either 1) spend their money (which is what the Fed wants) or 2) reach for a higher yield in other places (stocks, bonds, etc.). Since this is a post about emergency funds we'll quickly discourage you from doing 1) and let Grandpa Buffett address 2). Referring to the cash he was bequeathing to his son as an emergency fund, in 1939 he said:

You might feel that this should be invested and bring you an income. Forget it -- the mental satisfaction of having $1000.00 laid away where you can put your hands on it, is worth more than what interest it might bring, especially if you have the investment in something that you could not realize on quickly.

And therein lies the key to the emergency fund. It needs to be liquid. DO NOT be tempted to invest in somewhat risky or longer term opportunities to grab a higher yield. As many found in 2008, higher yield almost always equals higher risk; many funds considered safe did not hold up when the excrement hit the air conditioning. As Ray Devoe put it, "more money has been lost reaching for yield than at the point of a gun." So, only consider bank accounts, CDs, bank money market funds, or reputable** money market mutual funds for your short term funding emergencies.

Now, how much should be placed in the fund? Three months of living expenses should be the absolute minimum. If your job is somewhat tenuous, hold six months worth. Remember to subtract your savings rate when calculating how much you need, as you won't be saving during a crisis. So, say you make $40k (after taxes) per year, while you usually save 15% of your money and want a 3 month fund. $40000 * (1-.15) / 4 = $8500. Now defer consumption, reach your number, park it (even at low interest), and sleep like a baby.

* Each year Buffett hosts thousands in Omaha at the annual shareholders meeting for his firm, Berkshire Hathaway. Despite the fact that it's dubbed the "Woodstock for capitalists," Benji has resisted my entreaties for such a high-minded road trip. Seems to have something to do with the arrival of his new son, who was incidentally named after the founder of Vanguard, Jack Bogle. (Edit: it appears that the naming may have been a coincidence).

** Reputable money market mutual funds are those that largely invest in government debt. Look for words like treasury, federal, govt backed, agency debt, and certificates of deposit. See here for a good candidate.

Tuesday, May 3, 2011

The likelihood of rare events

Take a 1000 year flood for example. The earth doesn't have a memory as such* and so even just 10 years after such an event there is still a small chance that it will have happened again. You'll also notice that after 1000 years it's not assured that the event will have occurred (cause it's only 1 in 1000 on average); even after 1500 years it only has a 77.7% chance of having happened.

The scary thing is the first part of the figure. By year 223 there's a 20% chance that the event has already occurred, and it's a 1 in 1000 yr event! So whether we're talking earthquakes, end of civilizations, floods, droughts, or whatever, these

The scary thing is the first part of the figure. By year 223 there's a 20% chance that the event has already occurred, and it's a 1 in 1000 yr event! So whether we're talking earthquakes, end of civilizations, floods, droughts, or whatever, these{kind=link}

One of the biggest planning mistakes people make is to treat the unlikely as impossible.^

*Technically, many environmental variables due show small autocorrelation (i.e., memory), but it depends on what we're dealing with. The zero autocorrelation assumed above is a reasonable simplification, since we don't have enough data on rare events to meaningfully estimate this complication. Higher autocorrelation would make the events cluster in time (as with the earthquakes we've seen in Japan).

^While he's unlikely the first, Larry Swedroe makes this point in his book and in the bogleheads forum.

^While he's unlikely the first, Larry Swedroe makes this point in his book and in the bogleheads forum.

Sunday, May 1, 2011

Of Marginal Utility and Pascal's Wager

To preface some of the material that will follow, it is important to think about how much happiness we receive from the money we are seeking. This is crucial in determining what to do in terms of personal financial decisions. For example, think about the principle of the marginal utility of wealth. This term from economics is simple to understand, yet has profound implications. It means that a dollar earned by a rich man will give him much less of a boost in happiness than a dollar earned by a poor man (notice the curved slope in this data). So, going forward, one has to consider the benefit of the positive increment of happiness, compared to the risk involved in achieving that expected return. Larry Swedroe explains:

While more money is always better than less, at some point most people achieve a lifestyle with which they are very comfortable. At that point, the taking on of incremental risk required to achieve a higher net worth is no longer acceptable to most people. The reason is that the potential damage of an unexpected negative outcome far exceeds the benefit that would be gained from incremental wealth. Thus each investor needs to decide at what level of wealth their unique utility of wealth curve starts flattening out.In the United States, and particularly with many of our socio-economic backgrounds, it is important to consider the way by which we can preserve what we already have (even if our portfolios are currently small or nonexistent). This is largely done through insurance and it's often quite inexpensive. Yes, we could save a few hundred dollars a year buying inadequate insurance and (in 30 years or so) we could be talking about a significant amount of money. People often justify this by thinking, well, how likely is it that I'll cause a multi-car crash (involving litigious people with nice cars) or have my house destroyed in an earthquake. But, it is essential that the consequences of our decisions dominate the probabilities of the outcomes. This is akin to Pascal's wager, wherein he explained that even though the existence of God cannot be determined through reason, one should take the bet and believe, nevertheless. William Bernstein explains it thusly: "If a supreme being doesn't exist, then all the devout has lost is the opportunity to fornicate, imbibe, and skip a lot of dull church services. But if God does exist, then the atheist roasts eternally in hell."

Basically, don't treat unlikely events as impossible and carefully consider the implications of such events. The downside potential you're exposing yourself to by skimping and saving money on insurance may not always manifest itself, but it might. Considering the uncertain world we here have to negotiate, you'll likely be better off saving money elsewhere.

See here for things you probably didn't know about happiness.

Subscribe to:

Posts (Atom)