You'll invariably hear that renting is throwing your money away, or that you're making the land lord rich, but people are often quick to ignore all the costs involved with homeownership. Proponents say that the tax break* is a real bargain or that house prices always go up and that you should get in while the gettin's good. The reality of it isn't so clear-cut. First, when buying a house one doesn't simply pay for the price of the house, but they pay what's called PITI (or, principle, interest, taxes, and insurance). This doesn't come cheap. Depending on the rate, interest can easily more than double the cost of your home. See this calculator for details on your situation (and hit the amortization button). Property taxes are usually a couple thousand per year (more if the house is large), and homeowners insurance often runs above $600 per year. This quickly looks onerous when compared to cutting a simple rent check each month (as renters insurance is often a nominal amount and the other fees mentioned are nonexistent). As a homeowner the ongoing costs quickly mount, as every extra square foot of the home has to be heated, cooled, maintained, repaired, insured, and taxed. Lately, we've added a few square feet. According to Robert Shiller, the "average size of new houses increased from 1100 square feet in the 1940s to 2150 square feet in 1997," just as family size has shrunk. With respect to these types of trends, Ben Franklin appropriately repeated the aphorism that "it is easier to build two chimneys than to keep one in fuel." After examining similar similar issues, Bill Bernstein, a respected financial theorist, concluded that "after taking into consideration maintenance costs and taxes, you are often better off renting." If you do buy, purchase the smallest house your family can stand.

Well, what gives? Just about everyone says buying a house is a wise move. In our culture whenever a young adult, fresh out of college, is at a family reunion, the older people perpetually encourage the youngin' to buy a house. They always say it's a great investment. But is it really an investment? Remember, investing is what we do after we've deferred consumption. As Bernstein avers, "Home ownership is not an investment; it is exactly the opposite, a consumption item." Do any recent homeowners out there feel as if they've actually been reducing their consumption?

If one does go ahead and considers it an investment, it is truly a poor one when assessed in light of three common characteristics which all good investments possess. First, for the vast majority, the home is often bought with a ton of borrowed money, which makes it a highly leveraged investment; this is bad. The gist: if you put 10% down on your house, your investment returns are magnified by 10 times (at 20% down they're magnified 5 times) This is how many people's equity was completely wiped out recently with price declines greater than 20% nationwide. - 20% X 5 or 10 quickly gets you to a 100% loss on your investment (i.e., you're underwater). A recent estimate states that over 28% of homeowners are underwater on their mortgages. Basically, these people have no skin in the game and their down payment (whatever it was) has been completely wiped out. The second negative characteristic is that your house is illiquid (i.e., you cannot get cash for it in a hurry). During a crisis people need quick access to cash. And it is exactly during crises that it's most difficult to sell your house or get a home equity loan. By contrast, the stock market is quite willing to buy your stocks from you at your leisure. Third, the purchase of a single home is undiversified. You're not investing in real estate in general, you're investing in a type of real estate (residential) in a very specific location. Again, the correlations here aren't helpful. Cities with the worst job situations will be the places where it's hardest to sell your house. Wanna uproots quickly and go to where the jobs are? Good luck. As Ryan Avent said, "homeownership, let's recall, is in most cases a highly leveraged, undiversified, relatively illiquid bet, with a return that is highly correlated to local labour market conditions."

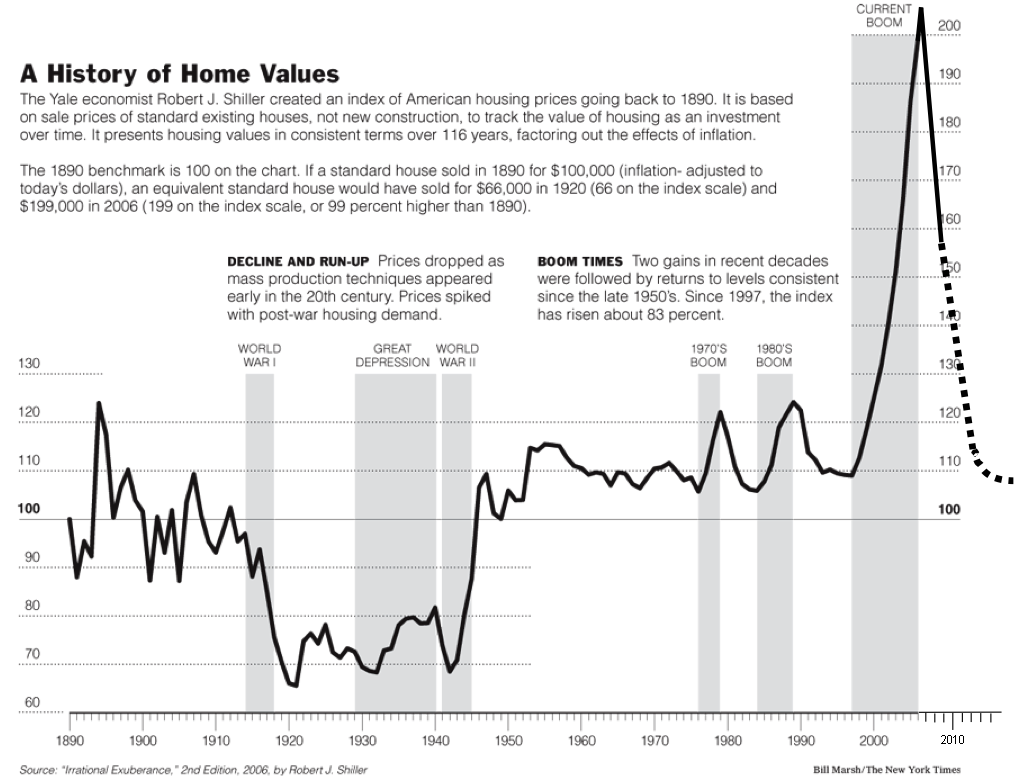

What about those high returns from price appreciation? They are largely illusory. Three studies of prices in the US, Norway, and Amsterdam show that our homes likely won't fund our retirement. First, Rober Shiller examined home prices back to 1890 and determined that, "until the recent explosion in home prices, real home prices in the United States were virtually unchanged from 1890 to the late 1990s." Note that this was written in 2006 and that real prices means that inflation is considered. Similarly, two bankers studied Norwegian house prices from 1819 to 1989 and found that their average real increase was 1.3% per year. Analogously, a Dutch finance professor analyzed transactions of buildings on one of the canals in Amsterdam from 1628-1974 and found that real prices there increased by 0.5% per year. Not exactly heady figures. Considering the price volatility, your money is probably better off invested elsewhere. Despite this, my (future) wife will probably want a house for the (future) kids and I'll likely be in the market for a place one day. But I won't consider it a wise financial move. Please comment and point me to views/articles that refute the above.

{kind=link}

*If one itemizes their taxes, they are able to deduct mortgage interest from their income. The benefits of this are debatable as most people don't itemize. Also, if you think it's a good deal to spend a dollar in order to get a quarter in return (how to think about the interest deduction), then message me cause maybe I'm missing something. The post above neglected to mention closing costs which often run at 6%. On a $200,000 home this is $12,000; this pain is often not felt as it's wrapped into the monthly payment.

** See here for a buy vs. rent calculator, here for what assumptions to use in the calculator, and here for a balanced view of this issue from the bogleheads, an online investing forum.

Levi, you've been riding this hobby horse for a long time, which is fine; I don't disagree with you. I do wonder though, how it is that you've managed to so completely ignore all of the benefits of owning a house--which have been pointed out to you, and by smarter minds than mine. (Something tells me that it might be because you have no experience as a renter, and less as a home-owner.) If you could address the opposing view (not that buying a house is an investment, but that it isn't the worst possible thing you can do--believe it or not, there are worse ways to spend your money) without the condescension, you might find yourself in a better (i.e. more persuasive) rhetorical position. Again, I don't disagree with you, but you're going about this the wrong way. But, whatever. Mostly I'm just excited for you to blame all of your poor financial decisions on women.

ReplyDeleteMike, most people are aware of the benefits of owning a house, as society often trumpets them ad infinitum. People are less aware of the downsides, which is why I wrote this. But, I agree, it would be good for me to address the benefits in a post as perhaps I'm discounting them. While I rented in Japan and have helped my widow mother administer the affairs of her house, my experience here is admittedly less than yours. What, in your time of living in these two situations, have you garnered in terms of financial knowledge that would render any of my post inaccurate?

ReplyDeleteI did, however, want to focus on the financial side of things (whether positive or negative), as that's where my problem is with regards to the prevailing views. I don't doubt that a house provides many non-financial benefits.

ReplyDeleteLevi, it seems to me that you ignore the costs of renting to reach a conclusion that is too broad. If you rent, you don't have to pay taxes, insurance, repairs, etc. But, your landlord does. And, any rational landlord is going to cover those costs--plus profit and administrative expenses--through rent. Likewise, let's accept that home ownership will not fund retirement -- neither does rent. Further, even if it is true that in most cases home ownership is not an investment -- in all cases renting is not an investment. Finally, real prices for homes may not increase, but rent prices are likely to increase with inflation.

ReplyDeleteI'd argue the issue is not home ownership. If you had a stable job, had no plans of moving, and were offered an opportunity to lease a property for $500/month (with the lease being renegotiated annually) or could buy the same property by obtaining a mortgage with total payments of $475/month, which would you choose? While I agree that the tax benefit is not reason to keep a mortgage you otherwise could pay off, in this scenario it is icing on the home ownership cake.

Ignoring all of the non-financial rewards, the real point seems to be not to buy a home that is larger or more expensive than is reasonable/needed. But the same would be true of renting a home/apartment that is larger or more expensive than is reasonable/needed.

Levi, in my comment, I indicate in two separate places that I don't disagree with you--I'm not implying that anything you say is "inaccurate." I AM saying that your perspective is intentionally limited. Granted, this is a blog about finance; however, by ignoring every other aspect of the issue, you've limited your perspective to the point that it is distorted. The result is that, occasionally, you drift into Michal Moore's school of reporting only what is convenient for your argument.

ReplyDeleteI think that Mitch's final assessment of the post is right on and complements the themes of previous posts on this blog, specifically the Thoreau: try not to allow your wants to out-pace your means.

Here's a question for you: what does the world start to look like as fewer and fewer people buy homes--it's happening, but what does it mean? Do fewer and fewer people start to own more and more property? This isn't a criticism, it's a question: how does this change society? What are the consequences? Greater financial independence, or (enter hyperbole) the return of a kind of feudalism/serfdom?